While South Africa’s inbound tourist arrivals continue to move beyond pre-pandemic figures, with total arrivals in February exceeding 2019 levels, overseas markets are still in recovery mode.

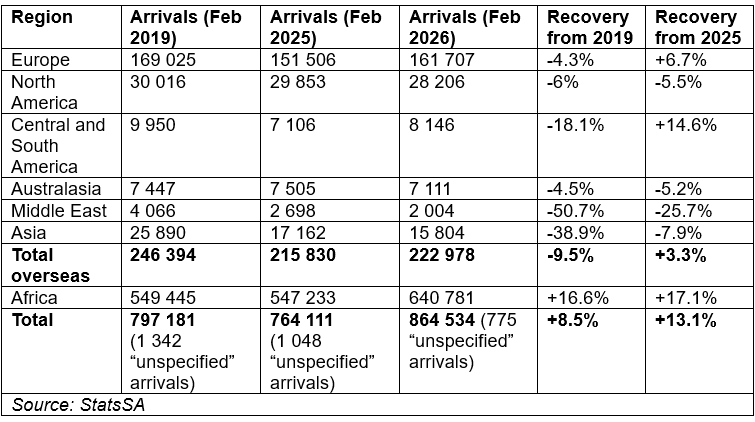

According to the latest International Tourism Report from Statistics South Africa (StatsSA), total arrivals reached 864 534 in February 2026 – a 13.1% increase on February 2025 and 8.5% higher than February 2019.

However, this is largely fuelled by Africa, which recorded 640 781 arrivals in February.

In contrast, total overseas arrivals reached 222 978 – up just 3.3% on 2025 but still 9.5% below 2019 volumes.

Europe remains South Africa’s largest overseas source market with arrivals at 95.7% of 2019 levels and 6.7% higher than 2025.

However, performance across other regions is more uneven.

Asia and the Middle East continue to lag significantly behind pre-pandemic benchmarks, recovering to just 61.1% and 49.3% of 2019 levels, respectively. Both regions also declined compared with February 2025.

The Americas present a mixed picture. North America is stabilising, with arrivals just below 2019 and 2025 levels, while Central and South America showed strong year-on-year growth although still well short of pre-pandemic volumes.

Australasia is also close to full recovery compared with 2019 but recorded a slight dip versus 2025.

Here is the full breakdown:

Cracks remain in key markets

David Frost, CEO of SATSA, told Tourism Update that February’s arrival figures are encouraging but the fact that total arrivals are now exceeding pre-pandemic levels largely on the back of African markets, although positive, does not tell the full story of tourism growth.

“Regional travel remains important, particularly for business, MICE, medical, study, VFR and shopping segments. However, the higher-value opportunity still lies in overseas markets where travellers stay longer, spend more and travel more widely through the country. It is not about prioritising one market over another but about ensuring a diverse mix of tourism streams supports growth and strengthens the economy.”

Frost said the latest source market data shows that recovery remains uneven.

“Germany (114.6%) and the Netherlands (115.3%) have moved ahead of 2019 levels while the UK (98.3%) is close to full recovery. France (81%) remains below pre-pandemic levels while the India (74%) and China (28%) markets continue to lag. African arrivals should not be discounted but neither should they mask underperformance in long-haul markets.”

Overall recovery year to date, comparing January and February 2026 with the same period in 2019, is 95.57%, up from 90% over the same period last year, Frost added.

“But the data must be read holistically. South Africa is a year-round destination with distinct seasonal patterns across source markets. Easter timing can also affect first and second quarter comparisons.”

At the same time, global volatility remains a factor.

“A recent SATSA survey found Europe showing the greatest level of travel disruption linked to the Middle East war while rising fuel and airline costs are also a growing concern. African and domestic travel will remain an important base but stronger, integrated source market plans will be critical if South Africa is to protect demand and convert recovery into sustainable long-haul growth,” said Frost.