South African hotel groups operating in the three- and four-star segments are facing significant challenges in maintaining occupancies and average rates at properties in Sandton and KwaZulu-Natal as hotels in Cape Town continue to thrive on the back of soaring demand.

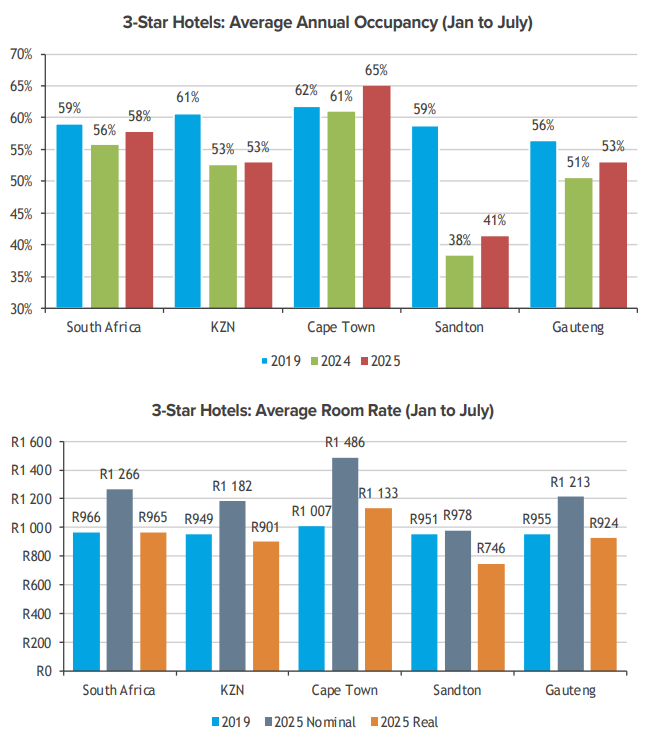

STR data analysed in BDO’s Tourism Trends Report shows that, between January and July this year, three-star hotels in Sandton recorded an average occupancy rate of 38% – a 21% drop from 2019 levels. Average room rate (ARR) decreased by 20% in real terms.

Properties in KwaZulu-Natal experienced an 8% decline in occupancy to 53% while ARR fell by 5%.

In the four-star segment, occupancies in Sandton (64%) and KwaZulu-Natal (68%) slightly exceeded 2019 levels but were accompanied by drops in ARR of 3% and 14% respectively.

In addition to changes in domestic business travel and government spending patterns, the three- and four-star segments (outside of Cape Town) have been plagued by waning demand from overseas tourists, said Lee-Anne Bac, Advisory Partner: Tourism at BDO South Africa.

“Our numbers have yet to return to 2019 levels and those that are visiting South Africa tend to avoid Gauteng and KwaZulu-Natal and/or are selecting five-star properties where they can get more bang for their buck.”

Challenging operating environment

Hoteliers told Tourism Update that BDO’s findings reflect in their portfolios.

“In both nodes, we have experienced a gradual softening in demand over an extended period rather than a sharp decline,” said Sigal Geva, COO at Premier Hotels & Resorts, which owns nine properties in KwaZulu-Natal and six in Gauteng.

Geva said KwaZulu-Natal has battled to recover from a series of compounded disruptions including severe flooding, water pollution and political instability.

“The knock-on effect has been more pronounced than initially anticipated, particularly within the domestic market segment, which remains under financial pressure,” said Geva, adding that international arrivals have not yet returned to pre-COVID levels.

“Where international guests are returning, we have noted a clear preference for leisure-oriented destinations, such as Cape Town, over business-heavy or provincial areas like Gauteng and KwaZulu-Natal. This aligns with broader market observations that many international travellers are selecting destinations where they perceive higher value and enhanced experiences,” Geva added.

In Sandton, budget constraints in private and public-sector business travel resulted in softer weekday occupancies and rate resistance, according to Geva.

“While these factors have influenced performance to an extent, Premier Hotels & Resorts has actively responded by diversifying our market focus and placing greater emphasis on leisure, sports and group travel segments while strengthening partnerships with trade, tour operators and corporate clients. These initiatives have helped to mitigate some of the negative impacts of broader market shifts.”

Corné Alberts, National Marketing Manager at ANEW Hotels & Resorts, confirmed that recovery across the group’s nationwide portfolio is uneven.

“Overseas visitors are gravitating towards the Western Cape while destinations such as Gauteng and KwaZulu-Natal continue to face headwinds due to infrastructure challenges, limited direct air access and lingering perceptions around safety and service reliability,” she said.

“These factors, combined with a global shift towards experiential nature-oriented travel, have concentrated international arrivals elsewhere but we are actively collaborating with tourism partners to re-energise these regions and showcase their value as part of South Africa’s diverse travel offering,” Alberts added.

Geva and Alberts said the growing availability of budget-friendly alternatives has added pressure.

“We have seen the effects of increased competition from alternative accommodation options, including short-term rentals and serviced apartments, which have gained popularity among leisure and extended-stay travellers,” Geva said.

Cape Town thrives

The picture is far healthier at mid-market Cape Town properties with ARR at three- and four-star properties up by 12% and 40% respectively, according to BDO’s analysis.

“Our Cape Town properties have mirrored this broader positive market trend, achieving strong occupancies and sustained rate growth. The strength of the Cape Town market has allowed us to maintain rate integrity and focus on yield optimisation rather than volume alone,” said Geva.

The destination continues to benefit from improved air access, strong destination marketing and a diversified visitor base of domestic and long-haul markets, Geva added.

“For Premier Hotels & Resorts, specifically, performance has been further supported by proactive internal strategies including our positioning within key nodes of the city, close collaboration with trade and tour partners, and a refined focus on international group and leisure business,” Geva said.