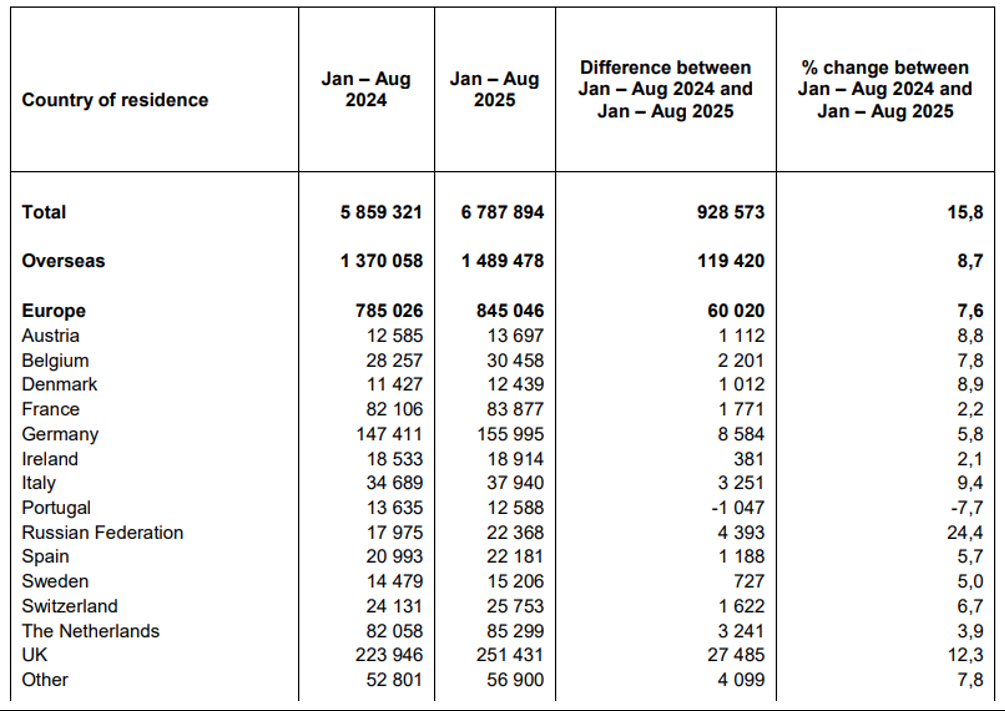

The European market accounts for almost 60% of all overseas arrivals in South Africa, illustrating the region’s continued importance in driving the country’s tourism performance.

SA Tourism has an extensive footprint across Europe, carrying out its destination marketing activities from hubs in UK/Ireland, Central Europe, South Europe and North Europe.

SA Tourism’s Regional GM for Europe Ian Utermohlen gave Tourism Update in-depth insights into the DMO’s marketing strategy, the barriers facing the market and forecasts for future performance.

What are the foundational aspects of SA Tourism’s strategies for targeting the European market?

When I started at SA Tourism in 2007, I was astounded at the research unit we have, versus what I saw in working for the private sector, in terms of understanding markets and gaining insights into the customer.

If we start at just the awareness level of South Africa as a tourism destination, we have an initial market of around 60 million people in key European source market countries. We then narrow this down to people who have sought information on travel to South Africa, which is around 10 million. The leakage points from this consumer base are quite high (due to factors such as the high costs of long-haul travel and personal safety considerations) so we narrow down further to just over four million consumers that we are targeting at any given time in partnership with trade distribution channels.

We already know that these consumers have gone through the brand journey, they’re seeking information and are seriously considering us along with possibly between three and seven other destinations, and this is where we’ve got to win them over.

Our marketing strategy has evolved to place greater emphasis on considerers as a key growth segment, while still valuing repeat visitors for their role in driving tourism across different parts of South Africa.

While Europe has recorded solid year-on-year growth in arrivals to SA, the market still remains more than 10% behind pre-COVID levels. What are some of the underlying reasons for this?

We have been very encouraged by the most recent stats, such as the 21% year-on-year growth from Europe registered in August, which show that the combined marketing efforts of SA Tourism and our trade partners have been effective.

It’s very important to note, however, that European airlift is at just 78% of pre-COVID 2019 levels. Airlines are still recovering from the obliteration they experienced during the pandemic and we still have lower frequencies along with aircraft production shortages. This has pushed up the costs of flights from Europe, which amplifies the challenges to appeal to travellers, particularly the middle market.

South Africa offers exceptional value for money for the international market but the first hurdle for the consumer is getting past flight costs. We know from our research that, as soon as tickets go beyond a certain price, we lose some travellers who opt to go to Asia or other markets. The loss of SAA in Europe has had a significant impact. We used to have double daily flights to Heathrow, and flights to Frankfurt and Munich that have been taken out of the system and decreased competitiveness on routes. I’m hoping that, in SAA’s next rounds of investments, they come back and see the value in the UK and Europe.

On a positive note, the growth rate in arrivals is accelerating and markets such as the UK are currently steaming ahead. We need to focus on a balance between pure volumes and spend too. Overall, in 2023, foreign direct spend from Europe exceeded 2019, reaching just under R32 billion (US$1.84 billion). This declined in 2024 due to higher costs of air tickets, which contributed to a decrease in average length of stay from 15 days to 14 days. When you add that up, that was a lot of revenue lost when visitors were in the country.

We also lost a lot of experts selling South Africa during COVID and have a lot of new people within the distribution channel. So it’s an ongoing priority for us to train them on the destination and give them the confidence to sell because many of them may be perceiving the same barriers as consumers on the brand journey.

What are your predictions for the performance of the European market for the remainder of 2025 and into 2026?

Firstly, if I look at the data, we were sitting at an 8% year-to-date growth rate in arrivals from Europe at the end of August so it’s encouraging to see that we’ve come out of the traditional quieter European summer season unscathed. Most of the aircraft load factors are sitting at 95% and, if it stays the same heading into the peak season, I believe we can get to a 10%-plus arrivals growth this year.

A lot of 2026 is going to depend on airlift increasing back to 2019 levels. If SAA comes back in some form, this could help push us to beyond 2019 arrivals. Our source markets are diversified: growth is coming from multiple European markets, which is giving us confidence. But we always openly say that sustaining demand isn’t just about SA Tourism. It’s the private sector, the provinces, our missions in-country, everything we do together as Team South Africa that will position us for the future.